Consumer Loan vs Commercial Loan, Consumer and commercial loans are distinct financial instruments catering to different needs and entities. While consumer loans primarily serve individuals for personal expenses, commercial loans are tailored for businesses and organizations. Understanding the disparities between these two types of loans is crucial for making informed financial decisions. Let’s delve into the specifics of each and explore their disparities.

What Are Consumer Loans?

Consumer loans, as their name implies, are financial instruments provided to individuals to address their monetary requirements. These loans are generally unsecured, implying they need more collateral backing, although secured alternatives are also available.

Within the realm of consumer loans, a variety of common types exist, such as personal loans, auto loans, mortgages, and credit cards. These instruments serve as vital resources for individuals seeking to fund diverse needs, whether purchasing a vehicle, acquiring a home, covering unexpected expenses, or managing day-to-day financial transactions.

The accessibility and flexibility of consumer loans empower individuals to navigate various financial situations and achieve their goals effectively.

Types Of Consumer Loans

Consumer loans encompass diverse options, each meticulously crafted to meet distinct needs. Take personal loans, for example—they boast versatility, catering to expenses like debt consolidation, home improvements, or medical bills.

On the other hand, auto loans are finely tuned to facilitate vehicle purchases, boasting meticulously structured repayment plans. Whether consolidating debts, enhancing living spaces, or addressing healthcare needs, personal loans offer financial support.

Similarly, auto loans streamline acquiring vehicles, ensuring borrowers can access reliable transportation while adhering to manageable payment schedules. Essentially, consumer loans present tailored solutions tailored to individual requirements, empowering borrowers to navigate financial challenges confidently and easily.

Benefits Of Consumer Loans

Consumer loans present numerous benefits to individuals. They offer swift access to funds devoid of the need for collateral, rendering them ideal for addressing emergencies or unexpected expenses that may arise. Additionally, consumer loans frequently boast competitive interest rates, ensuring affordability for borrowers with commendable credit scores. This accessibility and affordability make consumer loans favourable for those seeking financial assistance, enabling them to address immediate needs without undergoing the cumbersome process of providing collateral. Hence, individuals can use consumer loans to navigate financial challenges effectively while benefiting from favorable terms tailored to their creditworthiness.

Learning Commercial Loans

Commercial loans, conversely, cater specifically to the needs of businesses and commercial entities. These financial instruments fulfill a wide array of purposes essential for business growth and sustenance, encompassing endeavors such as expansion initiatives, procurement of necessary equipment, securing working capital for day-to-day operations, and acquiring real estate properties vital for establishing a physical presence or expanding operations.

Commercial loans come in both secured and unsecured forms, with the distinction often hinging on the borrower’s creditworthiness and the lending institution’s risk assessment policies. This flexibility allows businesses to access the capital required to pursue their strategic objectives while accommodating varying financial circumstances and risk appetites.

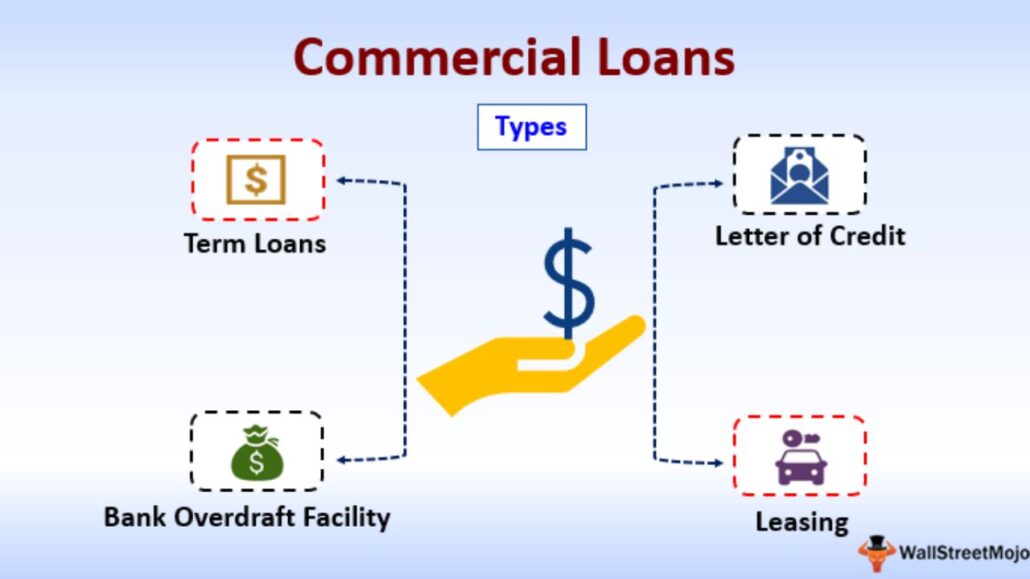

Types Of Commercial Loans

Commercial loans cover a broad spectrum of financial solutions designed specifically to address the distinct requirements of businesses. Term loans involve receiving a fixed amount of money repaid over a set timeframe, catering to various business needs. On the other hand, Small Business Administration (SBA) loans represent a form of financing supported by the government, particularly beneficial for small enterprises.

Additionally, lines of credit and commercial mortgages stand out as prevalent options within commercial loans, providing businesses with flexible access to funds or opportunities for property acquisition. These diverse offerings ensure businesses of all sizes and industries can find suitable financial support to fuel their growth and success.

Advantages Of Commercial Loans

Commercial loans provide numerous benefits to businesses, providing a pivotal resource for accessing substantial capital essential for their growth and expansion endeavors.

By availing themselves of commercial loans, companies can embark on various strategic initiatives such as investing in new ventures, procuring vital equipment, or acquiring valuable real estate properties. Moreover, these loans frequently come with advantageous interest rates and flexible repayment terms, empowering businesses to efficiently navigate their financial obligations.

This enables them to allocate resources strategically, optimize cash flow, and confidently seize growth opportunities, thereby fostering sustained success and competitiveness in their respective industries.

Key Differences Between Consumer And Commercial Loans

While consumer and commercial loans serve distinct purposes, they differ significantly in various aspects.

Purpose

Consumer loans are intended for personal expenses such as education, healthcare, or vehicle purchases, whereas commercial loans are utilized for business-related purposes like expansion, inventory financing, or operational expenses.

Eligibility Criteria

The eligibility criteria for consumer loans primarily depend on the individual’s credit score, income, and debt-to-income ratio. In contrast, commercial loans may require extensive documentation, including business plans, financial statements, and collateral.

Interest Rates

Consumer loans typically have lower interest rates than commercial loans, reflecting the lower risk associated with individual borrowers. Commercial loans, especially those without collateral, may carry higher interest rates to compensate for the increased risk.

Repayment Terms

Consumer loans generally have shorter repayment terms ranging from a few months to several years, depending on the loan amount and type. Commercial loans, however, may offer longer repayment periods, aligning with the business’s cash flow and revenue generation.

When To Opt For A Commercial Loan?

Businesses ought to contemplate the utilization of commercial loans when they find themselves in need of capital to fuel growth endeavors. Such initiatives may encompass broadening operational capacities, acquiring essential equipment, or venturing into real estate investments.

Acquiring a commercial loan provides businesses with the essential financial resources for grasping expansion opportunities, thus bolstering their competitive edge within the market.

By leveraging commercial loans, businesses can effectively finance strategic ventures that enhance productivity, efficiency, and market presence. Ultimately, opting for a commercial loan empowers businesses to embark on transformative endeavors that propel their growth trajectory and solidify their position in the competitive landscape.

Risks Associated With Consumer Loans

While consumer loans offer advantageous opportunities, they also harbor inherent risks necessitating borrower vigilance. Among these risks lies the peril of accumulating substantial debt, particularly when borrowers misuse or exceed the intended scope of loan funds.

Additionally, defaulting on payments for consumer loans poses a grave threat to both credit ratings and overall financial stability. This dual jeopardy underscores the importance of borrowers exercising caution and prudence when engaging with consumer loans, ensuring that financial decisions align with their capabilities and circumstances. By remaining aware of these risks and proactively mitigating them, borrowers can navigate the borrowing landscape more effectively and safeguard their long-term financial well-being.

Risks Associated With Commercial Loans

Commercial loans pose significant risks, especially for businesses, with one prominent concern being the potential for overleveraging. This occurs when a business accumulates excessive debt, leading to constraints on profitability and impeding overall growth prospects.

Additionally, economic downturns or fluctuations in the market further compound these risks, as they can directly affect the business’s capacity to meet its loan obligations. Such scenarios increase the likelihood of default, presenting a substantial risk factor for businesses relying on commercial loans for financing. Hence, prudent financial management and risk assessment are imperative for businesses to mitigate these potential pitfalls associated with commercial borrowing.

Importance Of Research And Due Diligence

When contemplating the acquisition of either a consumer loan or a commercial loan, it is imperative to engage in comprehensive research and due diligence. Potential borrowers must diligently compare available loan options, meticulously evaluate interest rates and terms, and thoroughly assess their financial standing before finalizing loan agreements.

A thorough understanding of the terms and conditions outlined in the loan agreement is paramount to preempt any unforeseen challenges or pitfalls that may arise throughout the borrowing process. By diligently conducting research and exercising prudence in decision-making, borrowers can confidently navigate the loan acquisition process and secure the most suitable financial solution for their needs.

Factors To Consider Before Choosing A Loan

When individuals and businesses contemplate borrowing, it’s imperative for them to meticulously weigh a plethora of factors to ascertain that the chosen loan resonates harmoniously with their financial aspirations and prevailing circumstances.

These pivotal factors encompass but are not limited to the loan quantum, interest rates, repayment modalities, associated fees, and any supplementary perks or advantages proffered by the lender.

By diligently assessing these variables, borrowers empower themselves to make discerning and well-informed choices regarding their borrowing endeavors. Such a comprehensive evaluation ensures that the selected loan aligns seamlessly with their financial objectives and safeguards against potential pitfalls or mismatches that could impede their financial well-being in the future.

Real-Life Examples

To illustrate the practical application of consumer and commercial loans, let’s consider a few real-life examples:

Consumer Loan Case Study:

A recent college graduate Sarah decides to take out a personal loan to consolidate her student loan debt. By consolidating her loans, Sarah can simplify her monthly payments and potentially lower her interest rate, saving money over time.

Commercial Loan Case Study:

XYZ Corporation, a small manufacturing company, applied for a commercial loan to purchase new equipment for its production facility. The loan will help XYZ Corporation modernize its operations, improve efficiency, and meet increasing customer demands.

Expert Insights And Recommendations

Financial professionals stress the significance of cautious borrowing and meticulous strategizing concerning both consumer and commercial loans. They advocate for a thorough evaluation of one’s financial standing, a thorough exploration of available alternatives, and, when necessary, seeking counsel from experts before finalizing any loan agreements.

This advice underscores the critical nature of making informed decisions to ensure financial stability and mitigate risks associated with borrowing. By heeding these recommendations, individuals and businesses can navigate the complexities of loan acquisition with prudence and foresight, safeguarding their financial well-being and optimizing their borrowing experiences for long-term success.

Conclusion

Consumer loans and commercial loans fulfill unique objectives and target distinct entities. Consumer loans are specifically crafted to address personal financial needs, covering expenses such as education, healthcare, or major purchases. On the other hand, commercial loans are tailored to facilitate the growth and expansion of businesses.

Recognizing the disparities between these loan categories and their respective risks and advantages is paramount for individuals and businesses to make well-informed financial choices. Individuals can effectively manage their finances by understanding the nuances of consumer and commercial loans, while businesses can strategically leverage financial resources to propel their growth trajectories.

FAQ

What Are The Main Differences Between Consumer Loans And Commercial Loans?

Consumer loans primarily target individual expenses, encompassing personal purchases or unexpected emergencies. In contrast, commercial loans serve the specific needs of businesses, facilitating endeavors such as expansion initiatives or acquiring essential equipment. This clear distinction delineates the distinct purposes of each loan type, catering to the divergent financial requirements of individuals and enterprises.

How Do Eligibility Criteria Vary Between Consumer And Commercial Loans?

Consumer Loan vs Commercial Loan, Consumer Loan vs Commercial Loan, Consumer loans typically focus on an individual’s credit score, income, and debt-to-income ratio, whereas commercial loans may require extensive documentation including business plans, financial statements, and collateral.

What Are The Risks Associated With Consumer Loans?

Consumer loans come with inherent risks, such as the possibility of accumulating significant debt, experiencing negative impacts on credit scores, and facing financial instability in the event of missed payments. These risks underscore the importance of responsible borrowing and diligent repayment to mitigate potential adverse consequences and safeguard one’s financial well-being.

What Factors Should Businesses Consider Before Opting For A Commercial Loan?

Consumer Loan vs Commercial Loan, Before selecting a commercial loan, businesses must carefully evaluate several key factors. These include the loan amount, interest rates, repayment terms, fees, and most importantly, the potential impact of the loan on their cash flow and profitability. By thoroughly assessing these elements, businesses can make informed decisions that align with their financial objectives and ensure the sustainability of their operations.

How Can Borrowers Mitigate Risks Associated With Both Consumer And Commercial Loans?

Consumer Loan vs Commercial Loan, Reducing potential hazards entails engaging in comprehensive research, evaluating various loan alternatives, comprehending the loan terms thoroughly, and evaluating one’s financial capacity before entering into a loan contract. By diligently examining these aspects, borrowers can make informed decisions and mitigate the likelihood of encountering unforeseen challenges or financial difficulties throughout the loan tenure.

{kind=link}